New confirmation of the VAT treatment of chain sales where the intermediate buyer-reseller is in charge of the intra-Community transport of the goods

Background

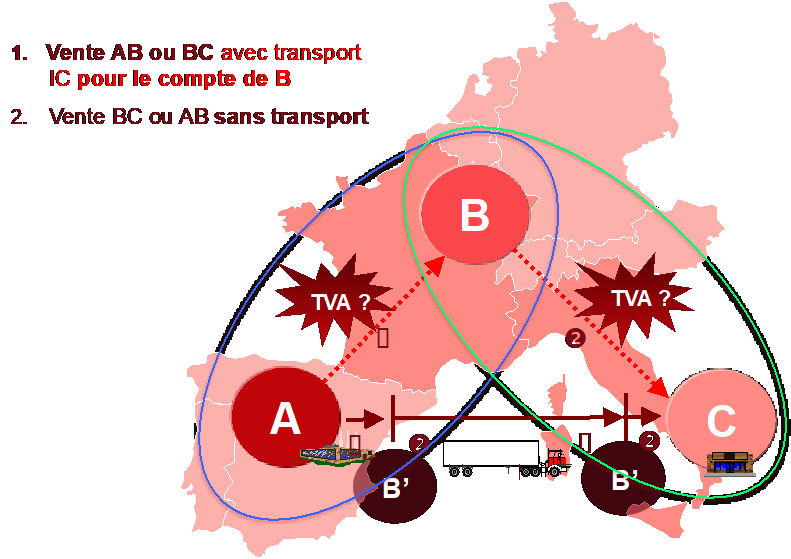

The European Court of Justice (ECJ) recently confirmed the exemption conditions applicable to the first supply made within the framework of cross-border chain sales (e.g. triangular transactions) where intermediate buyer-resellers (e.g. a trading company ‘B’ in chain sales between businesses A-B-C) are in charge of the intra-EU shipment of the goods. In this case, the key point is whether the intra-EU transport made by or on behalf of B should be ascribed to his purchases (e.g. under incoterms EXW, FOB, FCA where the point of delivery of the first supply A-B is in the first EU member State) or to his sales.

In this respect, the ECJ case law makes a distinction depending on whether B in the relation A-B-C takes the goods out of the first Member State before or after the goods are resold to C (i.e. whether C placed an order to B before the latter takes out the goods from the EU member State of departure) and, if C placed an order, whether A is informed of the fact that goods are already resold before they leave the first EU member State.

In the Euro Tyre Holding case (CJUE 16 December 2010, C-430/09, Euro Tyre Holding BV), the ECJ considered that the supplier (A) can in principle exempt the supply to B if the latter expressed his intention to transport the goods outside the EU Member State and provide to A a VAT number granted by another EU member State. However, according to the Court, A “might be held liable to VAT on that transaction if he had been informed by that person of the fact that the goods would be sold on to another taxable person before they left the Member State of supply and if, following that information, the supplier omitted to send the person acquiring the goods a rectified invoice including VAT” (cf point 36). This is why the Court makes a distinction depending on whether B “had received a request to supply goods from the final purchaser before acquiring those goods from his supplier” or not (i.e. no prior order has been placed by the final purchaser) (cf point 22).

More recently, the ECJ confirmed that “Article 138(1) of the VAT Directive must be interpreted as meaning that (…) a supply of goods by a taxable person established in a first Member State is not exempt from VAT under that provision where, prior to entering into that supply transaction, the person acquiring the goods, who is identified for VAT purposes in a second Member State, informs the supplier that the goods will be resold immediately to a taxable person established in a third Member State, before he takes them out of the first Member State and transports them to that third taxable person, provided that that second supply has in fact been carried out and the goods have then been transported from the first Member State to the Member State of the third taxable person. (…)” (ECJ case C‑386/16 of 26 July 2017, Toridas UAB).

On the basis of the above case law, A can exempt the supply to B and the latter can apply the simplification for triangular transactions only if goods are either not already resold at the time they leave the EU Member State of departure or, at least, if it could be demonstrated that the supplier (A) was not aware that goods are already resold at the time the goods leave this Member State.

If B is able to support that the supplier is not aware that the goods are resold to a third party the simplification for triangular transaction could apply. The same goes if incoterms were e.g. DDP, CPT, CFR where the point of delivery of the first sale is outside the EU Member State of departure, as the supplier (A) would then take care of the intra-Community transport.

Our remarks

This case law highlights the complexity of identifying the regime applicable to the first delivery of a chain sale, the risks for the seller of wrongfully exonerating the delivery even though he is informed that the goods leave the territory and that the purchaser acts under a number assigned by another Member State, and the risks for the intermediate buyer-dealer to have to register for VAT purpose in the Member State of departure to declare his intra-Community supplies and to not be able to use the simplification measure for triangular operations. It is also planned to simplify the chain sales regime as part of a “quick fix” system that would occur in principle by 2020 (see news below).

We strongly recommend to examine the consequences of the above ECJ case law on the basis of an audit of your flows of goods, invoices and incoterms. We can help you to assess the steps to be taken with a view to both secure and optimize the VAT treatment of your transactions.

Need more information?